Downsizer Contribution: How to Boost Super Without Hurting Your Pension

If you’re over 55 and thinking about selling your home, the downsizer contribution could be one of the most powerful retirement strategies available.

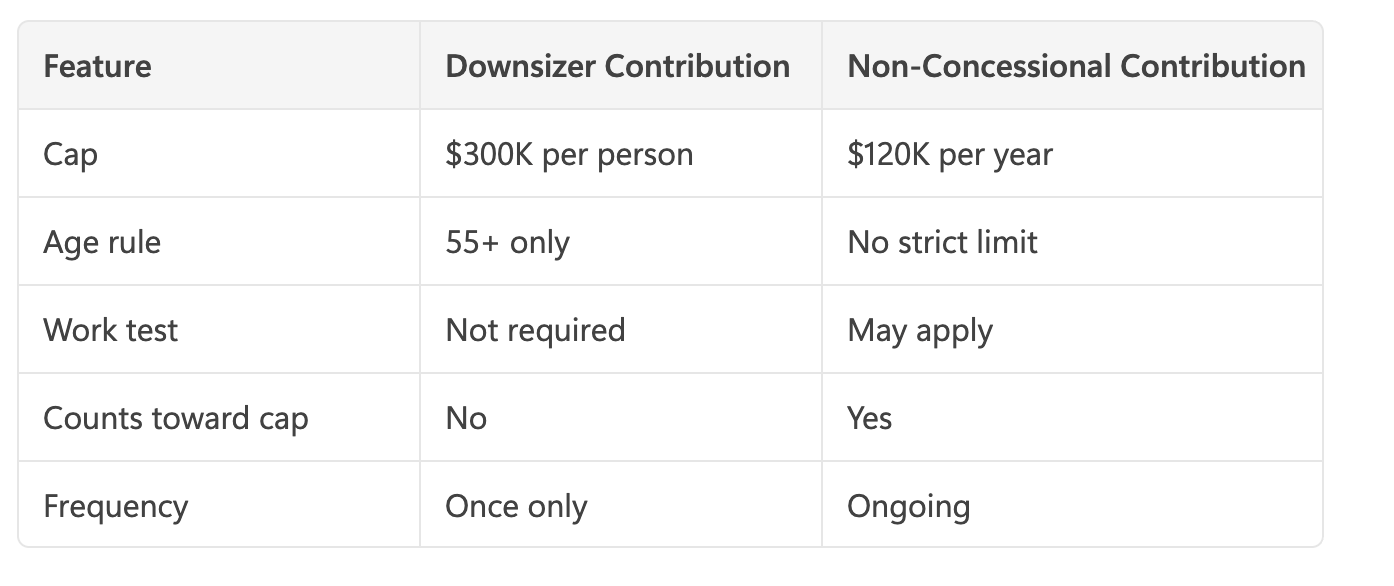

It allows you to move up to $300,000 per person (or $600,000 per couple) from your home into superannuation—without the usual contribution limits.

But there’s a catch: if done incorrectly, it can reduce or eliminate your Age Pension.

This guide explains exactly how it works, who it suits, and how to use it safely.

What Is the Downsizer Contribution?

The downsizer contribution is a special superannuation rule that allows Australians aged 55 or older to contribute proceeds from selling their home into super.

Key features:

Up to $300,000 per person

Available to couples ($600,000 combined)

Does not count toward normal contribution caps

No work test required

This strategy effectively allows you to convert property wealth into retirement income.

👉 For a deeper look at how downsizing itself impacts your pension, see

Selling the Family Home: Impact on Age Pension and Alternatives

Who Is Eligible?

To qualify, you need to meet strict criteria:

Basic eligibility:

Aged 55 or older

Owned the property for at least 10 years

The home qualifies for CGT main residence exemption

Contribution made within 90 days of settlement

👉 Downsizer contributions are typically a once-in-a-lifetime opportunity, so planning matters.

How the Downsizer Contribution Affects Your Age Pension

This is where most Australians go wrong.

The biggest misconception is:

“If I put the money into super, it won’t affect my pension.”

That is NOT true after Age Pension age.

Assets Test Impact

Once funds enter super AND you are of pension age:

The amount becomes assessable under the assets test

It can reduce or eliminate your pension

👉 Learn how this works in detail:

Assets Test Explained (2026 Guide)

✅ Example:

Sell home → $600K surplus

Move $600K into super

Your assessable assets increase significantly

Pension may reduce or stop

Income Test and Deeming

Centrelink doesn’t look at actual returns.

Instead, your assets are deemed to earn income, which affects the income test.

👉 Detailed breakdown here:

Income Test Explained (2026 Guide)

Key Rule – The Lowest Pension Applies

Centrelink uses both tests, and whichever gives the lower result applies.

👉 Read more:

Income vs Assets Test – Which Matters More?

How to Use the Downsizer Contribution Strategically

Used correctly, this strategy can:

Improve cashflow

Increase tax efficiency

Maintain or even improve your Age Pension

Strategy 1 — Timing Your Contribution

After selling your home:

Proceeds intended for your next home can be exempt for up to 12 months (or longer in some cases)[agepension...ces.com.au]

This creates a critical planning window.

Strategy 2 — Don’t Put Everything Into Super

Many retirees assume they should maximise contributions.

That’s often a mistake.

Instead consider:

Keeping some cash outside super

Paying off debt

Spending on exempt assets

👉 More ideas:

Can I Spend My Money and Increase My Age Pension?

Strategy 3 — Use the Family Home Advantage

Your home is exempt from the assets test, but cash is not.

👉 Understand this critical difference:

How the Family Home Affects Your Age Pension[agepension...ces.com.au]

Strategy 4 — Combine with Other Asset Strategies

The downsizer contribution works best alongside:

Super structuring

Asset repositioning

Gifting strategies (within limits)

👉 Learn more:

How to Reduce Assets for Age Pension Eligibility

Before you sell your home or make a downsizer contribution, it’s critical to model the impact properly.

Even small structuring changes can mean the difference between:

Keeping a full pension

Losing tens of thousands per year

👉 Book A Consultation Today

Downsizer Contribution vs Other Super Contributions

👉 Downsizer contributions are unique because they bypass normal restrictions.

Real-Life Example

John and Mary (Age 68)

Home sold: $1.2M

New home: $700K

Surplus: $500K

They:

Contribute $300K each into super

Total: $600K added

Result:

Super increases significantly

Assets test kicks in

Age Pension reduces

👉 As explained here:

Using the Downsizer Contribution Without Losing Your Pension

With proper structuring, however, the outcome could have been improved.

Benefits of Downsizer Contributions

✅ 1. Boost Super Quickly

Convert home equity into liquid retirement assets.

✅ 2. Tax-Effective Investing

Super earnings taxed up to 15% (or 0% in pension phase).

✅ 3. No Contribution Limits

Does not affect standard caps.

✅ 4. Simpler Income Planning

Allows structured drawdown strategies.

Risks and What Could Go Wrong

❌ 1. Losing Your Age Pension

Large contributions increase assessable assets.

❌ 2. Poor Timing

Making contributions before using exemption windows.

❌ 3. Liquidity Issues

Too much locked in super.

❌ 4. Not Reporting to Centrelink

👉 Important obligations explained here:

When Your Circumstances Change

When Downsizer Contributions Work Best

This strategy is most effective if you:

Are asset-test constrained

Want to simplify your finances

Need more tax-effective income

Have excess home equity

When It May NOT Be Suitable

It may not suit if you:

Are close to losing your pension

Need liquidity

Plan to gift money

Haven’t planned the tax implications

Related Strategy: Selling Property for Pension Improvement

👉 If you’re considering other property strategies, read:

Should You Sell an Investment Property?

Frequently Asked Questions

1. Can I make a downsizer contribution if I’m still working?

Yes. There is no work test for downsizer contributions. You can continue working and still contribute, provided you meet eligibility rules such as age and property ownership conditions.

2. Does the downsizer contribution affect the Age Pension?

Yes. Once funds are in super and you’re over pension age, they are counted under the assets test and deemed under the income test, which may reduce your pension.

3. Can couples both use the downsizer contribution?

Yes. Each partner can contribute up to $300,000, meaning a combined total of $600,000 can be contributed from the sale of a shared home.

4. Do I have to buy a smaller home?

No. Despite the name, you don’t have to downsize. You simply need to sell a qualifying home and meet eligibility criteria.

5. Is the downsizer contribution taxed?

No. It is made from after-tax proceeds and is not taxed when entering super. However, future earnings are taxed depending on the phase.

6. Can I use this strategy more than once?

No. Generally, you can only make a downsizer contribution once in your lifetime, even if you sell multiple properties later.

Conclusion

The downsizer contribution is one of the most powerful — and misunderstood — retirement strategies in Australia.

Done correctly, it can:

Boost your retirement income

Improve tax efficiency

Simplify your financial position

Done poorly, it can:

Reduce or eliminate your Age Pension

Lock funds into the wrong structure

Create long-term cashflow problems

Before selling your home or moving money into super, get personalised advice.

Your Age Pension outcome can change dramatically based on timing and structure.